The Four Stages of FIRE: Lean, Barista, FIRE, and Fat

Most people treat financial independence as a single, distant finish line: one big number you cross, after which you never have to work again. That framing is intimidating, and it is also misleading. FIRE is not one milestone. It is a series of them, and each one buys you a meaningful amount of freedom long before you hit the final number.

The FIRE community has settled on four milestones that mark distinct levels of financial security: Lean FIRE, Barista FIRE, FIRE, and Fat FIRE. Crossing each one changes how it feels to go to work on Monday morning.

In this article, I walk through what each milestone means, why the distinction matters, and how I track progress toward all four in Lume, a private, offline-first FIRE tracker for Mac.

Why think in milestones instead of one number?

When your only goal is “the big number”, progress feels invisible for years. You can save diligently for a decade and still feel like you have barely started, because you are measuring yourself against a target that is 80% away.

Breaking the journey into milestones fixes that in two ways.

It makes progress visible. Crossing your first milestone — knowing your investments could cover the basics if everything went wrong — is a genuine psychological shift. You are no longer starting from zero. You have built a safety net that most people never build.

It changes your decisions earlier. You do not need full financial independence to benefit from being closer to it. Each milestone gives you more leverage: the ability to take a pay cut for better work, to weather a layoff without panic, to say no to things you would otherwise tolerate. Freedom arrives gradually.

The math behind the first three milestones is the same — the 4% rule, which says you can safely withdraw about 4% of your invested net worth each year without running out of money over a long retirement. The only thing that changes between milestones is the size of the expenses you are trying to cover.

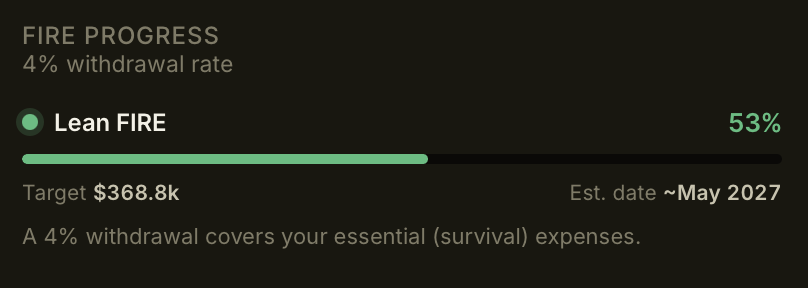

Lean FIRE

The first milestone is the point where a 4% withdrawal from your invested assets would cover your essential expenses — the things you genuinely need to stay alive and comfortable. Housing, food, utilities, insurance, basic transport. Not restaurants, not travel, not the nice-to-haves.

This is the most underrated milestone in the whole FIRE journey, and the one I wish more people talked about.

Reaching Lean FIRE does not mean you can quit your job and live your current lifestyle. It means something quieter but just as powerful: if you lost your income tomorrow, your investments could keep a roof over your head and food on the table indefinitely. Your basic survival is no longer dependent on your next paycheck.

That is an enormous amount of security. It turns a layoff from a crisis into an inconvenience. It lets you take risks — switching careers, starting something of your own, taking time off — that would be unthinkable when you are living paycheck to paycheck.

In Lume, this is why expenses are split into Survival and Non-essential categories during the monthly review. That split is not just bookkeeping — it is what makes Lean FIRE measurable. Lume knows your annual essential expenses, applies the 4% rule, and shows you exactly how close your net worth is to covering them.

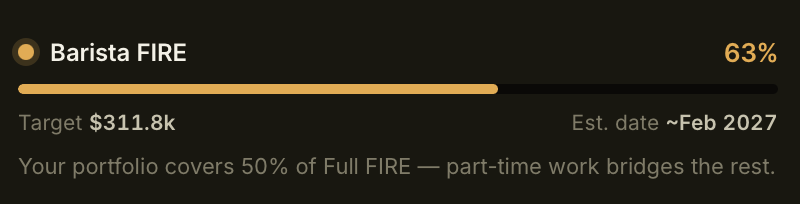

Barista FIRE

The second milestone sits between Lean and full FIRE, and it is one of the most practically useful points on the map. Barista FIRE is the point where your portfolio covers a meaningful fraction of your full FIRE target, and modest part-time income bridges the gap.

The name comes from the idea of working a relaxed part-time job — enough income to cover the remainder of your expenses, while your portfolio continues to grow untouched. You are no longer dependent on a demanding full-time career, but you have not fully stopped working either.

The appeal is that Barista FIRE arrives well before full FIRE, and the tradeoff is attractive: drop your working hours significantly, reduce stress, have time for the things that matter, and let compounding handle the rest. For many people, this is the real inflection point — the moment where work becomes optional in a meaningful way.

Lume tracks this milestone based on your current net worth relative to your full FIRE target. As your portfolio grows and the gap closes, you can see exactly how much part-time income would be needed to live comfortably today.

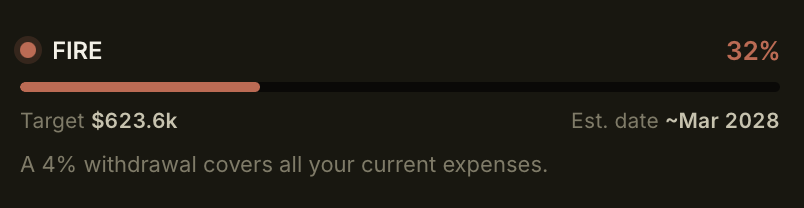

FIRE

The third milestone is what most people mean when they say “FIRE”: the point where a 4% withdrawal would cover your entire current lifestyle — essential expenses plus all the non-essential spending that makes life enjoyable.

This is the classic finish line. When you reach FIRE, you can stop working and maintain your life exactly as it is today, indefinitely, drawing down 4% of your portfolio each year.

The gap between Lean FIRE and FIRE is worth dwelling on, because it is entirely within your control. The difference between the two numbers is your non-essential spending. Someone with a lean lifestyle might find the two milestones are close together. Someone with significant discretionary spending will have a much larger gap — which is useful information in itself. It shows you, in concrete terms, exactly how much your lifestyle choices are extending your timeline.

Lume calculates this milestone from your total expenses (essential + non-essential), so as your spending changes over time, your FIRE target adjusts with it. That keeps the goal honest. There is no point chasing a number based on a lifestyle you no longer live.

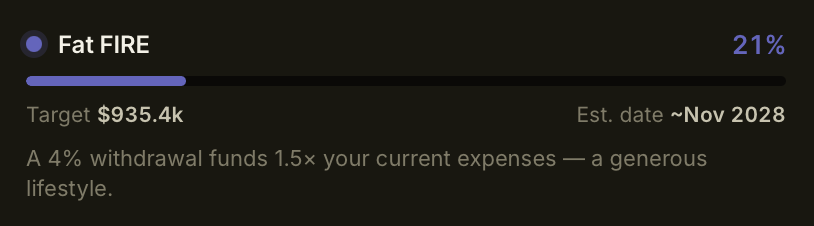

Fat FIRE

The fourth milestone is the most ambitious. Fat FIRE is the point where a 4% withdrawal funds a lifestyle beyond your current expenses — a generous margin that removes any anxiety about occasional splurges, inflation, or unexpected costs.

Where standard FIRE gives you enough to maintain your current lifestyle, Fat FIRE gives you room to upgrade it. It is less about reaching a precise threshold and more about the feeling that money has become a non-issue — you can travel more, give more, spend without second-guessing, and still leave a growing portfolio behind.

Not everyone targets Fat FIRE, and that is fine. For many people, FIRE is the real goal and Fat FIRE is a stretch ambition. But tracking it matters because it puts your FIRE number in perspective. If your current expenses are relatively lean, Fat FIRE may not be as far as you think. If you have been compressing your lifestyle to reach FIRE faster, this milestone shows you the cost of that compression — and whether the trade-off is worth it.

Watching all four at once

The thing I find genuinely motivating is seeing all four milestones on the dashboard side by side. They fill up at different rates, and that tells a story.

Early on, Lean FIRE climbs quickly — it is the smallest target, so every month of saving makes visible progress. Watching it approach 100% in the first few years is what keeps the habit alive when the final number still feels impossibly far away.

As Lean FIRE fills, your attention naturally shifts to Barista FIRE, then FIRE, then eventually Fat FIRE. You are never staring at a single bar that has barely moved. There is always a nearer milestone to chase, and crossing each one is a real, earned moment.

Even in months when the market dips and your net worth falls, a high savings rate keeps pushing all four bars forward. Once you see that relationship play out month after month, the whole journey stops feeling abstract.

Start tracking your milestones

You do not need to pick one milestone and ignore the rest. The point is to see all four at once, and to watch them progress month over month as part of your regular monthly review.

If you are on a Mac, Lume calculates all four milestones automatically from the data you already enter each month. No account, no subscription, no data leaving your machine.